HTX Options Trading Tutorial – European Spread options

- Options guides

What are European Spread options?

European Spread options are European-style options that help users realize an options strategy called vertical spread with ease. The strategy involves buying a call (put) and simultaneously selling another call (put) at a different strike price but with the same expiration. European Spread options allow users to set up a strike price interval to cap the profit potential in exchange for a lower premium. They are preferable to users who expect a moderate move in the price of the underlying asset.

Like American options, European Spread options offer two product types: Call and Put Spread, which reflect the user's view, bullish or bearish, on the underlying asset. Users who purchase European Spread options contract will make a profit if the underlying asset's price moves in their favor and the earnings from the options contract cover the paid premium. Though European Spread options cannot be exercised before the expiration date, users can sell the option in advance to lock in profits.

How to buy European Spread options?

1. Go to HTX’s official website: https://www.huobi.com/en-us/, move the cursor to “Derivatives” on the upper navigation panel, and click “HTX Options”. Or go directly to this link: https://www.huobi.com/en-us/otc-option/exchange

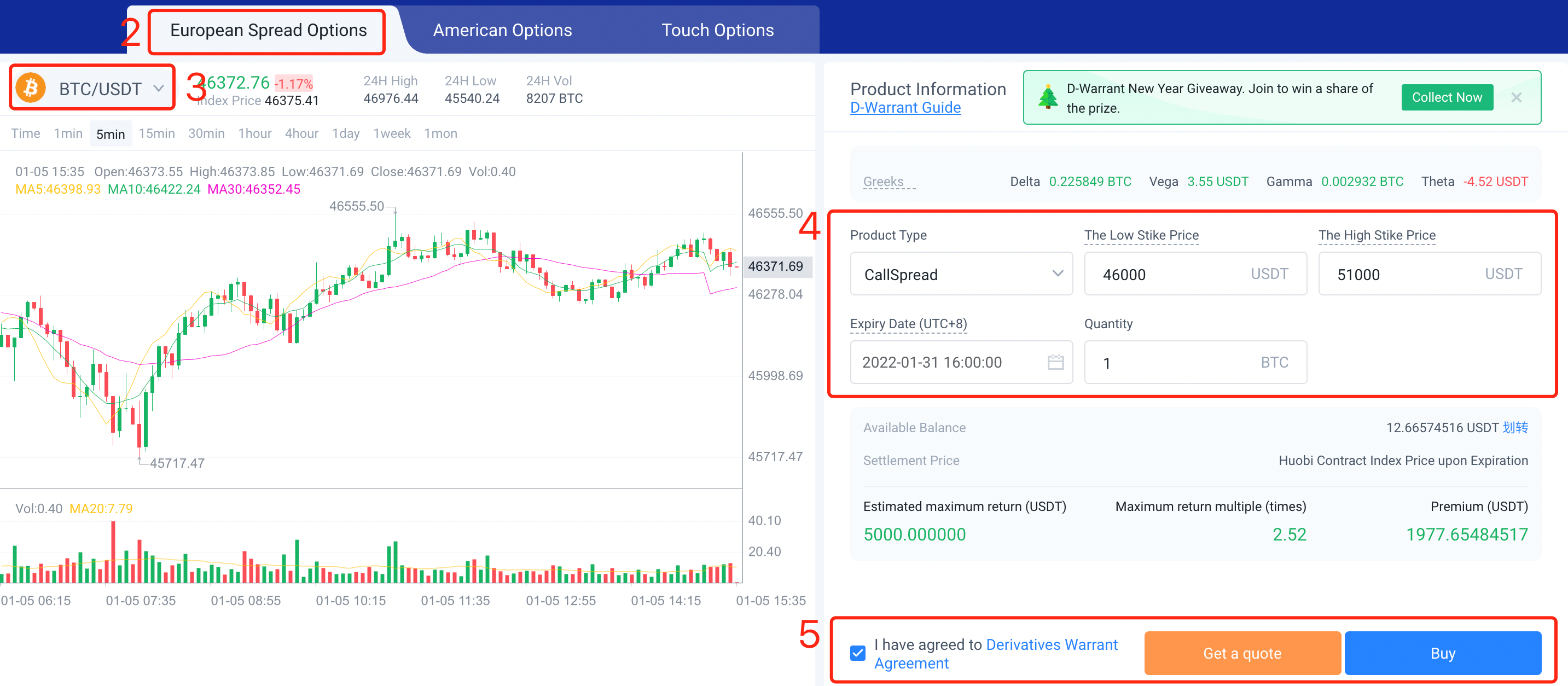

2. Click “European Spread Options” from the Option Selection Bar.

3. Click on the Asset icon located at the upper left corner to select the underlying asset of the options contract.

4. Set up European Spread options contract specifications, such as Call or Put Spread, High and Low Strike Price, Expiry Date, and Quantity.

5. Check the box to agree to the Options Agreement, click "Get a quote" to get a price offering for the options contract. If you think it’s a good deal, click “Buy” to purchase the options contract.

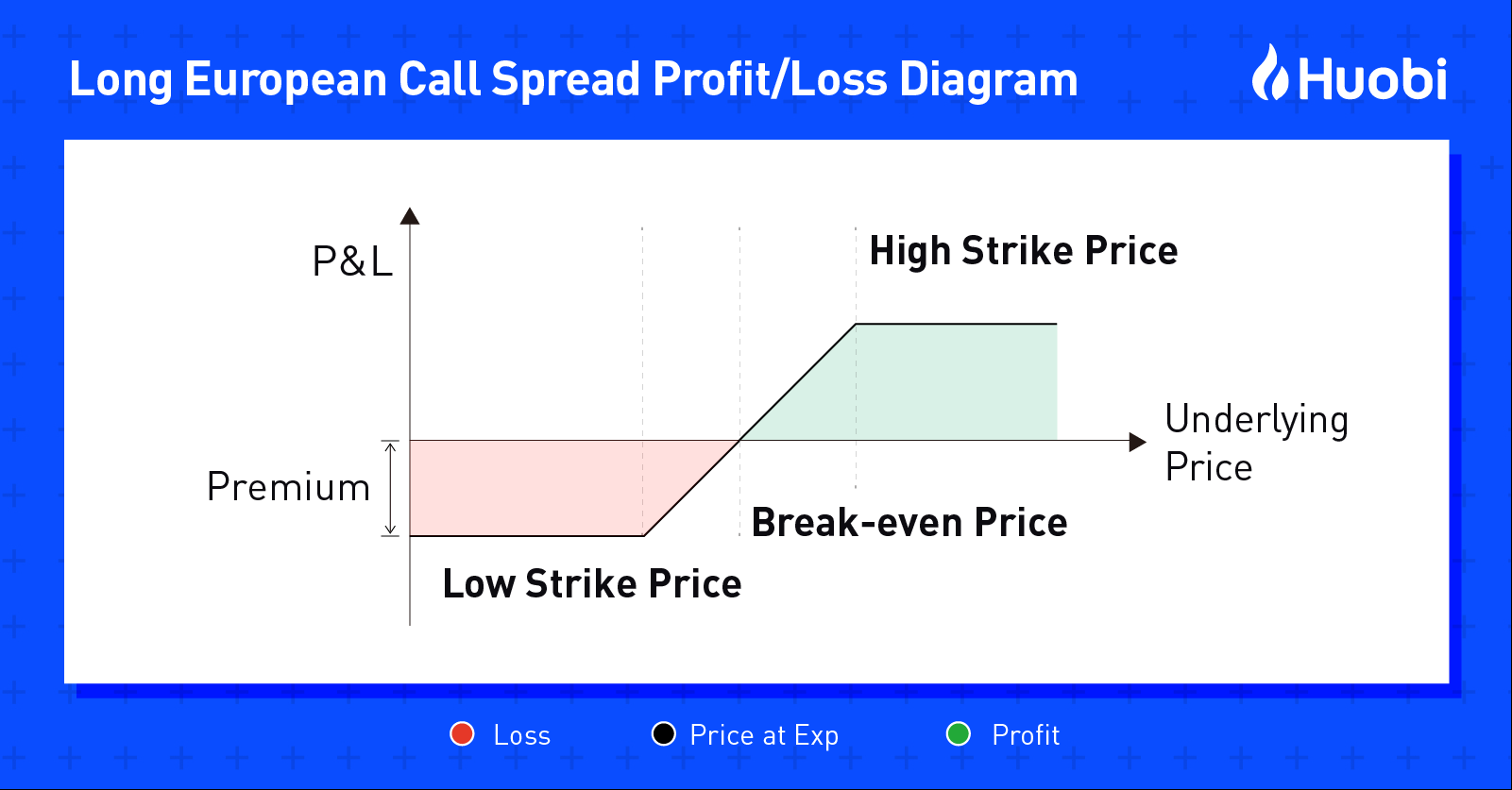

Call Spread

Call Spread options are for users who expect a moderate rise in the price of the underlying asset at expiration. With a Call Spread option, users can pay less premium than a vanilla call option, but their potential gain is capped once the price goes over the high strike price.

For a call spread option:

Max profit = the spread between the strike prices - premium paid

Max loss = premium paid

Break-even price (assume order quantity is 1) = low strike price + premium paid

At expiration,

If settlement price ≤ low strike price: payoff = 0

If settlement price > low strike price and ≤ high strike price: payoff = order quantity x (settlement price - low strike price)

If settlement price > high strike price: payoff = order quantity x (high strike price - low strike price)

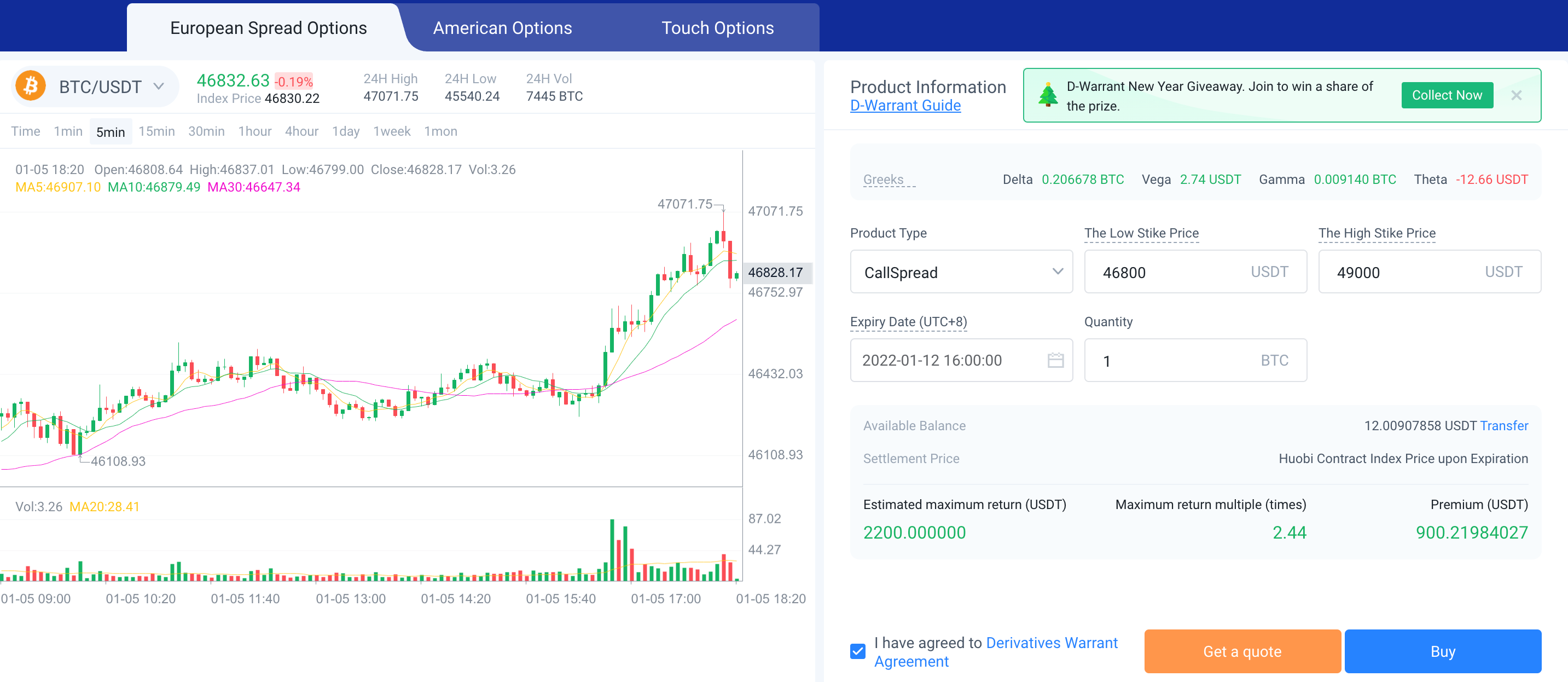

Case study for Call Spread

$BTC is currently trading at 46,832 USDT. Alexa believes the price of $BTC will rise, yet she doesn’t think the price will go over 49,000 USDT in 7 days. She buys a Call Spread option for 900 USDT with the following terms:

Low Strike Price: 46,800 USDT

High Strike Price: 49,000 USDT

Expiry Date: 7 days from today

Quantity: 1 BTC

Scenario 1: The market is very bullish. $BTC price rises to 51,000 USDT when the options contract expires. The price increase over the high strike price is irrelevant to this position. Alexa makes a profit of (49,000 – 46,800) – 900 = 1,300 USDT.

Scenario 2: $BTC price rises to 48,000 USDT when the options contract expires. Alexa makes a profit of (48,000 – 46,800) – 900 = 300 USDT.

Scenario 3: Alexa’s view on the market turns out to be wrong. $BTC price drops to 44,000 USDT when the options contract expires. Alexa receives nothing in return and loses 900 USDT.

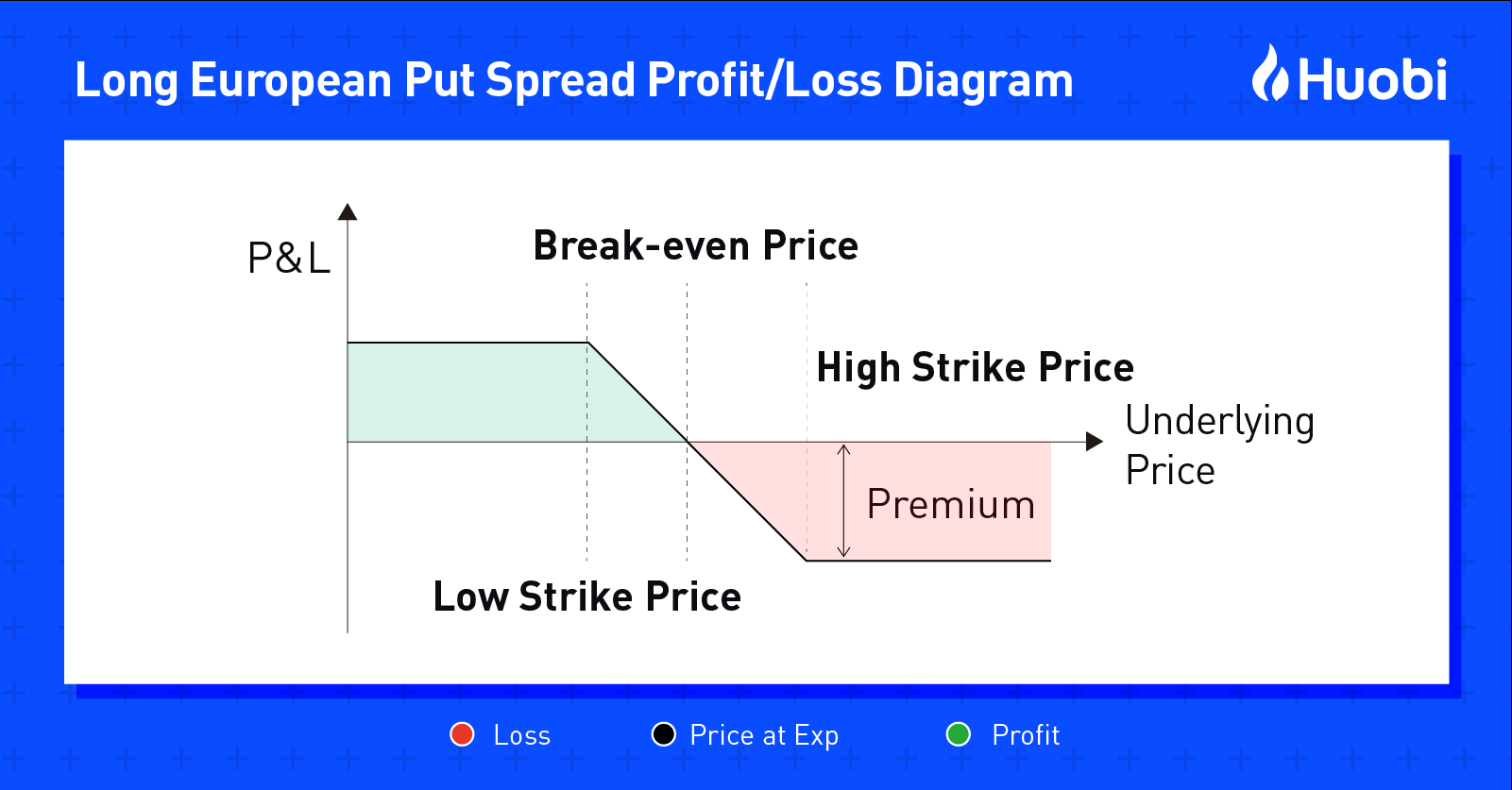

Put Spread

Put Spread options are for users who expect a moderate drop in the price of the underlying asset at expiration. With a Put Spread option, users can pay less premium than a vanilla put option, but their potential gain is capped once the price goes under the low strike price.

For a put spread option:

Max profit = the spread between the strike prices - premium paid

Max loss = premium paid

Break-even price (assume order quantity is 1) = high strike price - premium paid

At expiration,

If settlement price ≤ low strike price: payoff = order quantity x (high strike price - low strike price)

If settlement price > low strike price and ≤ high strike price: payoff = order quantity x (high strike price - settlement price)

If settlement price > high strike price: payoff = 0

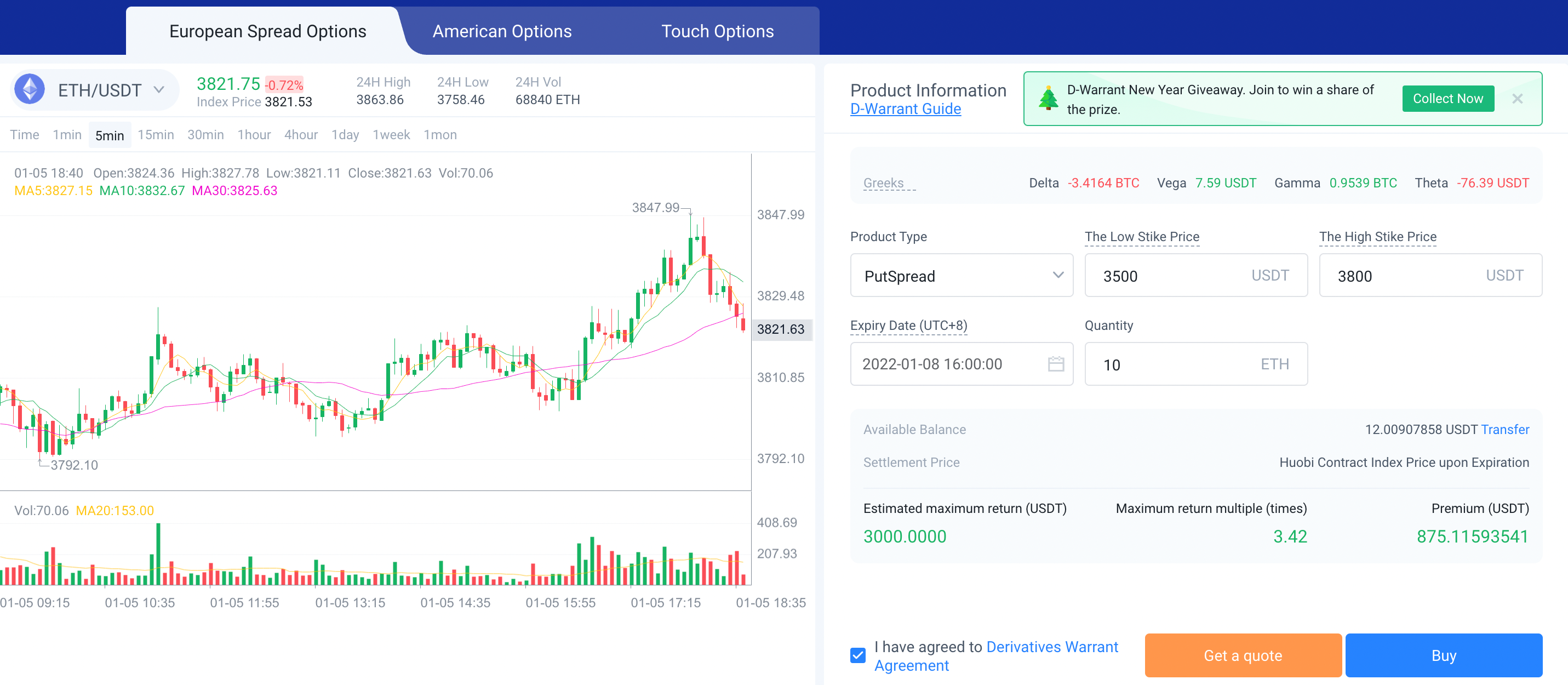

Case study for Put Spread

$ETH is currently trading at 3,822 USDT. Bob believes the price of $ETH will fall, yet he doesn’t think the price will drop below 3,500 USDT in 3 days. He buys a Put Spread option for 875 USDT with the following terms:

Low Strike Price: 3,500 USDT

High Strike Price: 3,800 USDT

Expiry Date: 3 days from today

Quantity: 10 ETH

Scenario 1: The market is very bearish. $ETH price falls to 3,400 USDT when the options contract expires. The price decrease below the low strike price is irrelevant to this position. Bob makes a profit of 10 x (3,800 – 3,500) – 875 = 2,125 USDT.

Scenario 2: $ETH price falls to 3,750 USDT when the options contract expires. Bob’s PNL is 10 x (3,800 – 3,750) – 875 = -375 USDT.

Scenario 3: Bob’s view on the market turns out to be wrong. $ETH price rises to 3,850 USDT when the options contract expires. Bob receives nothing in return and loses 875 USDT.

Some other things to know about European Spread options

Aside from the fact that European Spread options limit both risk and the return potential, they are much like European vanilla options. Longer time till expiration, higher implied volatility, more favorable strike prices, and a wider strike price interval will all lead to a higher options premium.

When a European Spread options contract is active, users can set up a target price to take profit. If a target price is set, the options contract is automatically sold when the underlying asset’s market price hits the target price.

Contact Us

Telegram: https://t.me/HTXOptions

Twitter: https://twitter.com/HTX_Options

E-Mail: [email protected]